Latest Competitive Analysis of Novartis Drug Pipeline

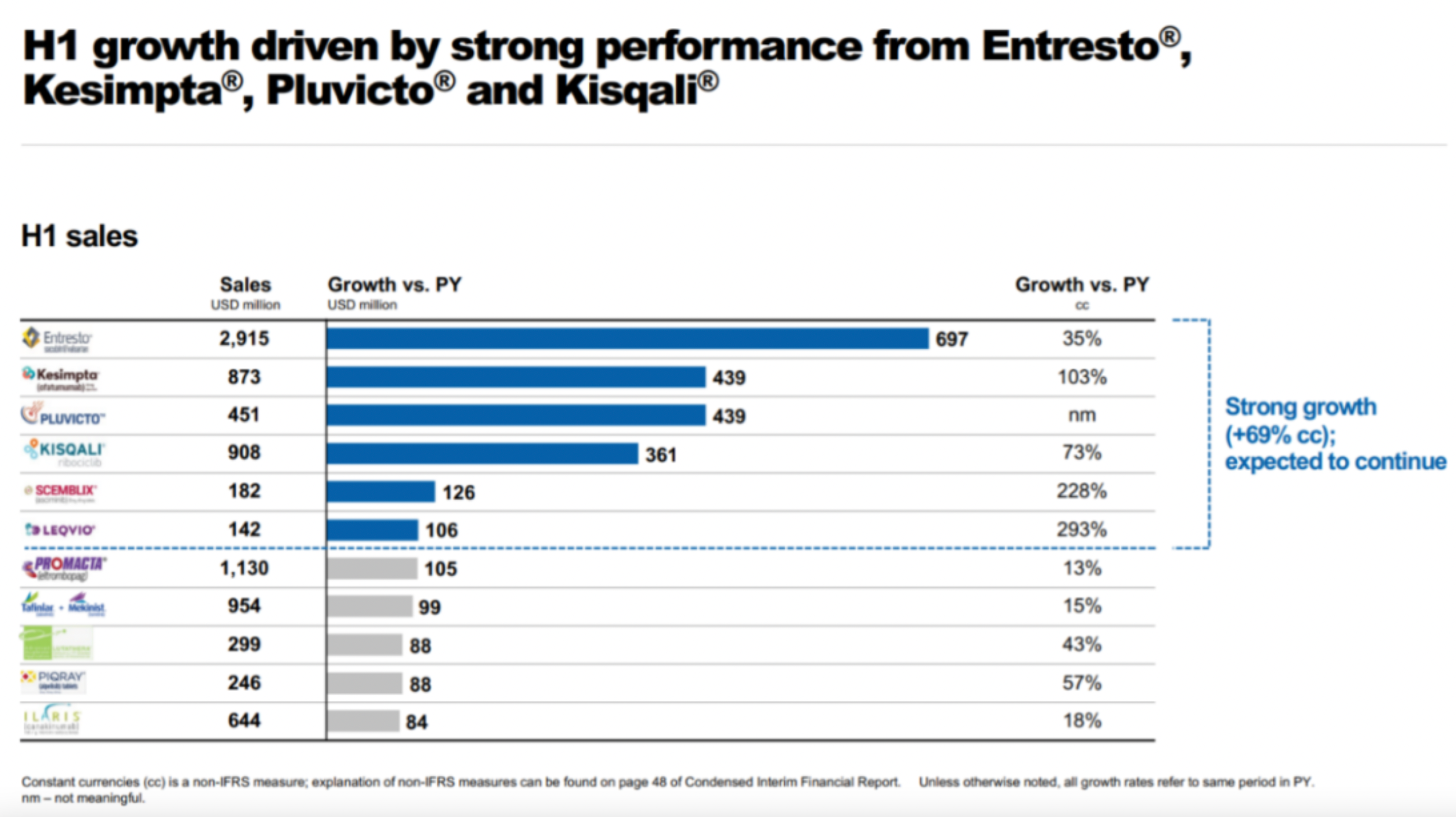

Despite Novartis being a consistent top contender in the pharmaceutical sector in terms of revenue, its growth and market value in recent years has been rather dismal.

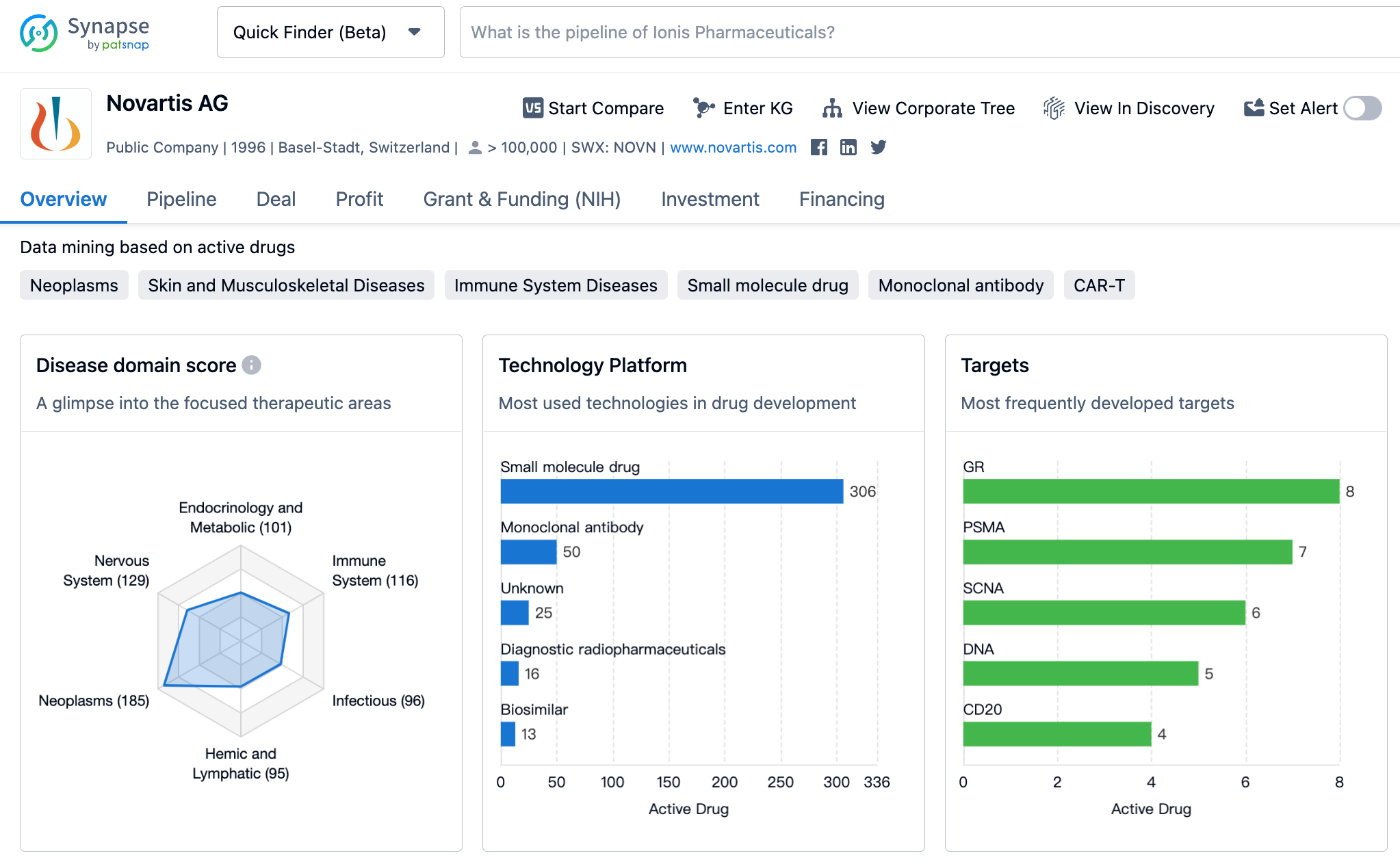

👇Please click on the image below to directly access the latest data (R&D Status | Core Patent | Clinical Trial | Approval status in Global countries) of Novartis.

On one hand, it has barely reaped any benefits from the pandemic (which also means it doesn't have to worry about a decline in performance now that the pandemic is fading). On the other hand, the company's investment in new modality in the past two years seems to have hardly paid off.

The reason why it hasn't paid off is because its main sources of income are still the old guard like Entresto, Secukinumab, Ofatumumab, and Ribociclib. The radioactive drug Pluvicto has been growing quite rapidly and should reach significant threshold this year, but the much-anticipated PCSK9 siRNA drug Inclisiran has been rather embarrassing, with quarterly sales not even crossing the $100 million mark.

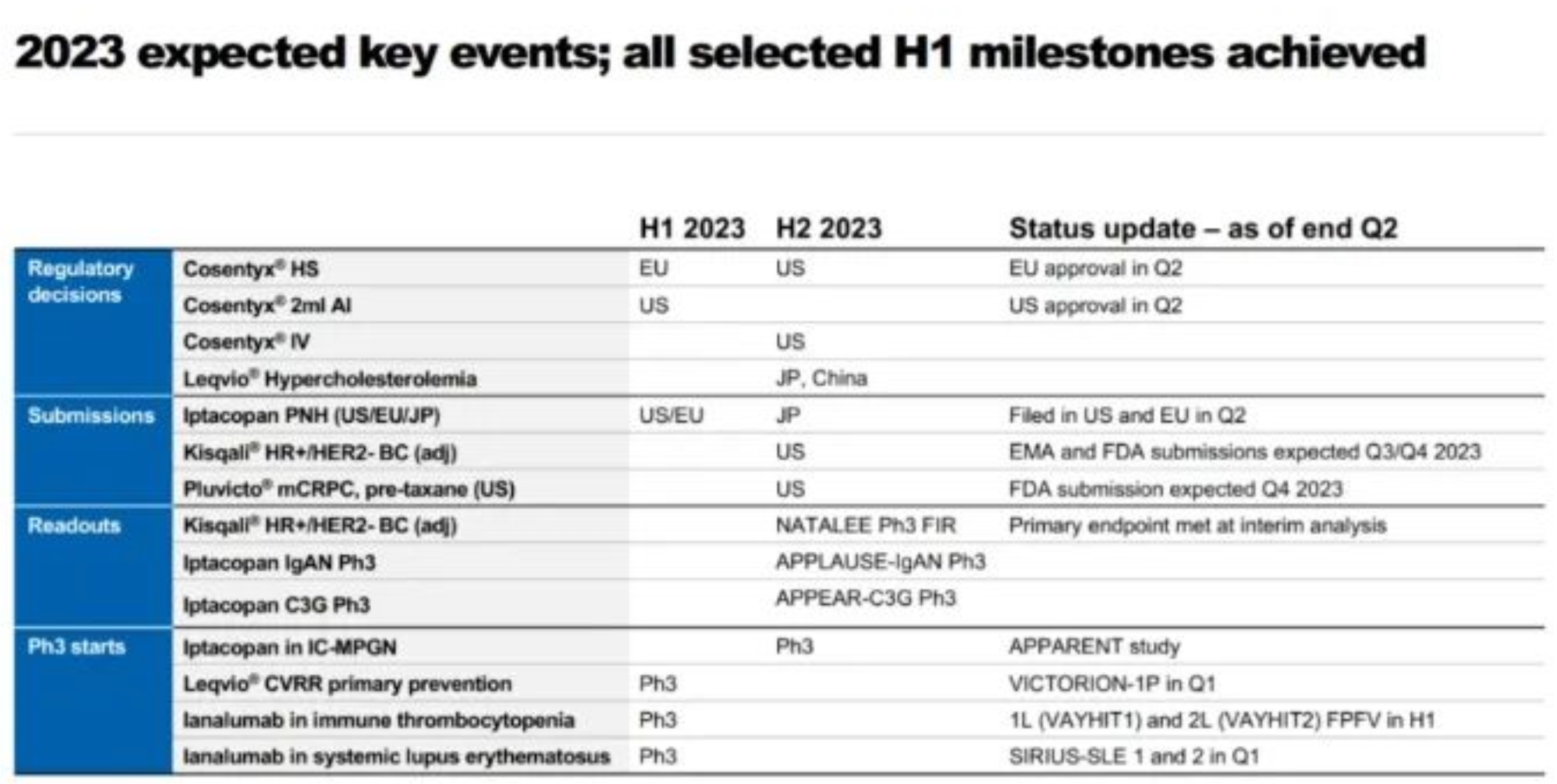

Its R&D efforts, too, seem rather pedestrian. Worth noting are the next-generation BTK inhibitor Remibrutinib reaching a primary endpoint in two Phase 3 trials for chronic spontaneous urticaria, the Phase 3 clinical results of the CDK4/6 inhibitor Ribociclib in combination with endocrine therapy for early breast cancer, the FDA's approval of PCSK9 small nucleic acid drug Inclisiran for expanded use in primary hyperlipidemia and NMPA approval for launch, as well as the approval of Secukinumab in Europe for the treatment of hidradenitis suppurativa.

However, there's no shortage of bad news, with the most important being the loss of the Entresto patent litigation in Delaware, and the launch of generic drugs from Chinese companies such as SQUARE Pharmaceuticals, along with the termination of the collaboration with BeiGene on the TIGIT monoclonal antibody Ociperlimab, and the cessation of development of the TGFβ monoclonal antibody NIS-793 for pancreatic ductal carcinoma indications.