Latest Competitive Analysis of Pfizer Drug Pipeline

In the wake of the receding tide of COVID-19 oral medication and vaccines, Pfizer seems to have returned to an awkward predicament where all potential growth points have fallen flat.

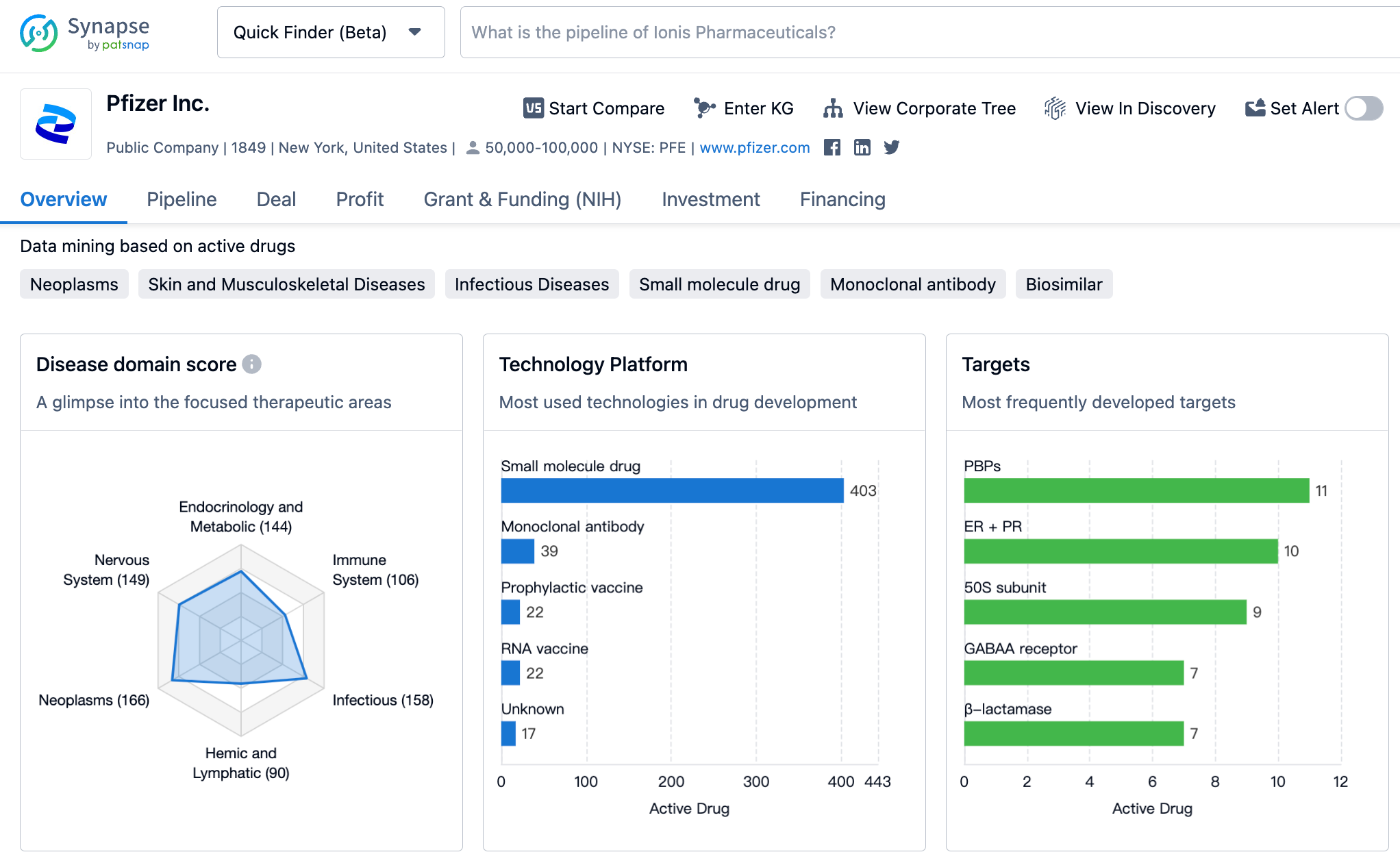

👇Please click on the image below to directly access the latest data (R&D Status | Core Patent | Clinical Trial | Approval status in Global countries) of Pfizer.

Palbociclib, Apixaban, Prevnar20 have all past their prime, and the only drug that shows a slight increase, Tafamidis, is merely a drop in the bucket. As a result, Pfizer’s market capitalization, which briefly reached over $300 billion in 2022, has recently returned to around $200 billion, causing Pfizer to drop to ninth place in the ranking of large pharmaceutical company market values.

Pfizer is now looking to achieve growth through acquisitions, aiming to purchase $25 billion in revenue by 2030.

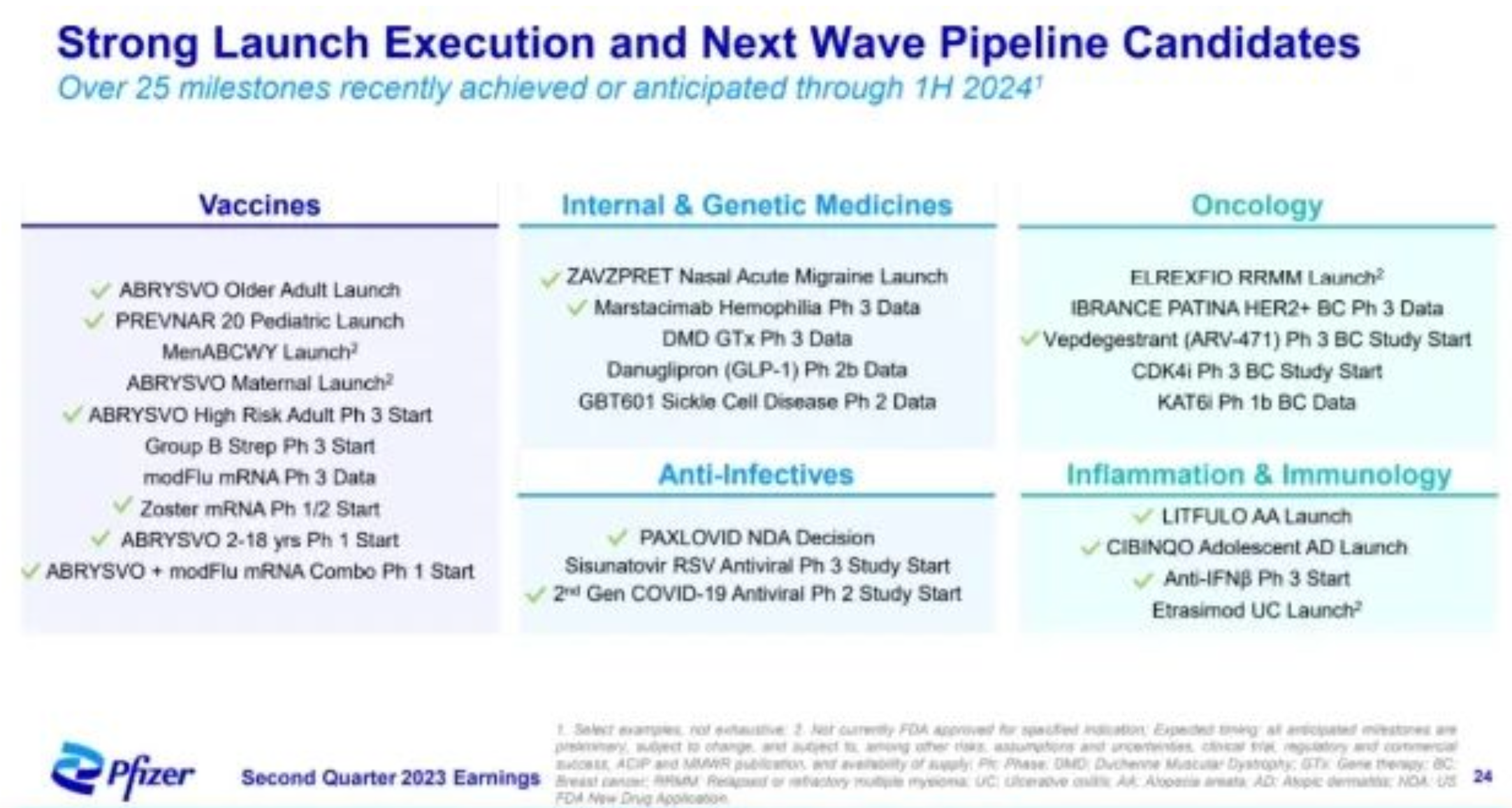

The most noteworthy recent R&D developments include the approval of the RSV vaccine and the CGRP migraine drug Zavegepant. Other noteworthy achievements include the approval of the BCMA×CD3 dual antibody Elranatamab, the approval of the JAK1 inhibitor Abrocitinib for adolescent Atopic Dermatitis indications, and the submission of applications for the S1PR modulator Etrasimod and the gene therapy SPK-9001. In addition, the Phase 3 clinical results for the Hemophilia drug TFPI monoclonal antibody Marstacimab have been released, and Pfizer decided between the two Oral GLP-1, abandoning Lotiglipron and pushing Danuglipron. While this long list may appear robust and impressive for a regular company, it seems somewhat insufficient for a top-tier pharmaceutical enterprise with a market capitalization in the hundreds of billions. It doesn't seem like there's anything that could form a strong pillar for rapid growth.